As part of the government’s budget announcement, it has proposed a number of key measures which are likely to impact employers:

- Worker status – changes to IR35 rules;

- National Living Wage and National Minimum Wage – increases;

- Employment termination payments – taxation regime; and

- Apprenticeship levy – reforms.

1- Worker status – changes to IR35 rules

The off-payroll working rules, commonly known as IR35, were introduced to ensure that individuals who work like employees pay broadly the same employment taxes as other employees, regardless of the structure they work through. Evidence suggests that only 10% of personal services companies (PSC) apply the rules correctly leading to a significant loss of tax revenue for the government.

In April 2017, reforms were introduced to address this issue in the public sector. The reforms moved responsibility for determining whether off-payroll rules apply from the PSC to the end user. As part of this process, HMRC introduced an online check on employment status for tax (CEST) to help end users determine status.

It has now been announced that from 6 April 2020, large and medium-sized businesses will be subject to the same off-payroll working rules as the public sector. Businesses will now be responsible for determining whether National Insurance contributions and income tax applies to their ‘self-employed’ contractors.

The policy encourages business to take a stringent approach to completing employment checks, as they could potentially face serious financial implications. This includes ensuring that the nature of the employment is accurately reflected in the contract and the correct form of tax is applied, particularly as the courts are concerned with the characteristics of the individual employment rather than the label given in the contract.

A further consultation will now take place on the operation of the new rules but businesses need to take steps now to audit and risk assess existing arrangements.

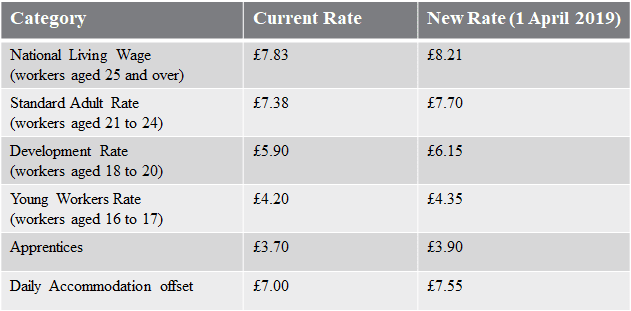

2- National Living Wage and National Minimum Wage – increases

From 1 April 2019 the following new rates will take effect.

3- Employment termination payments – taxation regime

On 6 April 2018, the government reformed the tax treatment of employee notice periods. Prior to this date, employers had greater scope to pay the equivalent of notice pay tax free (up to the £30,000 tax free exemption) where the employment contract did not contain a payment in lieu of notice clause (PILON). Under the new regime, all notice periods must now be fully taxed, even where a contract does not contain a PILON. This has increased the cost of exiting employees on enhanced terms of severance and has imposed some very complicated calculation methods on employers (See our webinar for further explanation).

As part of these reforms, it was also announced that any element of payment that exceed the current £30,000 tax free exemption, should be subject to employer Class 1A National Insurance contributions. This change was due to come into effect in April 2019. This date has now been postponed until April 2020.

4- Apprenticeship Levy – reform

The Apprenticeship Levy (Levy) was introduced in April 2017. The objective of the Levy is to fund new apprenticeships via employer contributions determined by levels of their payroll.

From April 2019, qualifying businesses will now be able to invest up to 25% of the Levy towards apprentices’ training and smaller employers will pay a reduced co-investment rate of 5% with the government paying the rest of the balance.

This will hopefully allow businesses to increase recruitment and complement the new training schemes introduced by the government. It is expected that ‘smaller employers’ will be confined to start-ups once the policy comes into effect.