Matthew Braithwaite

- Partner

- Private Client

An overview of the current considerations for US persons moving to or living in the UK in 2026.

Against a backdrop of global political and economic uncertainty, and despite significant recent changes to the UK’s tax regime for individuals, the UK remains an attractive and comparatively stable destination for internationally mobile Americans. This summary highlights the principal UK tax, immigration, investment and estate planning considerations for Americans relocating to, or already living in, the UK.

Immigration

The abolition of the UK’s investor visa in February 2022 brought to an end a popular immigration route for Americans moving to the UK. While it has been reported that the UK government is considering a replacement visa scheme, and is being heavily lobbied to do so, none has yet been announced. In the meantime, the current Global Talent visa (aimed at leaders in academic, arts, science and digital sectors) and Skilled Worker visa (self-sponsored or employer sponsored) are possible alternatives. American arrivers are therefore advised to take specialist immigration advice.

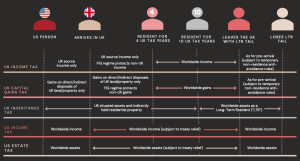

Tax for new arrivers

For US persons (FN1*) moving to the UK for the first time (and qualifying returners), the UK’s new 4-year Foreign Income and Gains regime (FIG regime) is likely to be attractive. The FIG regime was introduced from 6 April 2025, replacing the remittance basis of taxation. Broadly, US persons who have not been UK resident for at least ten consecutive UK tax years (FN2**) will be eligible to elect into the FIG regime for one or more of the first four consecutive years of UK residency with the consequence that:

US persons who become UK resident will however continue to be subject to US income tax on a worldwide basis and to ongoing US filing obligations. Fundamental distinctions between the US and UK tax systems (e.g. different tax years, rates and entity classification) can give rise to tax “mismatches” and double taxation, making coordinated UK and US advice essential.

Two structures which frequently cause difficulties are:

Such entities need to be reviewed carefully (ideally prior to relocation) to minimise the risk of double taxation.

Investments

Investments can give rise to similar tax “mismatches” due to differing tax treatment in the US and UK. This can give rise to issues for unwary investors. For example, UK tax‑advantaged investments such as ISAs, EIS/SEIS and VCTs offer no US tax benefits and may even create adverse outcomes for US persons. Non‑US funds including OEICs, unit trusts and foreign ETFs are classed as Passive Foreign Investment Companies (PFICs) for US purposes and attract punitive US tax treatment. A thorough review of investment holdings in advance of relocation is recommended.

Wills

It is often helpful for US persons who are residing in the UK to have an English Will dealing with UK‑situated assets (particularly UK real estate). This can allow a US person’s UK estate to be administered without awaiting a US grant of probate. Alternatively, any existing US Wills should be reviewed to ensure they operate efficiently from a UK perspective.

Once a US person has been UK resident for more than four tax years, their worldwide income and gains become fully taxable in the UK. Given the simultaneous US tax exposure, the US‑UK double tax convention will be central in managing the risks of double taxation for such individuals, their companies and trusts.

Long‑term residence rules

Since 6 April 2025, the UK’s “domicile” based test for inheritance tax, which was criticized for its uncertainty, has been replaced by a new “long term UK residence” (LTR) test. A person will be LTR and subject to inheritance tax on their worldwide estate if they:

Tax rates and exemptions

Inheritance tax is charged on death, and certain lifetime gifts, at current rates of up to 40% on sums in excess of the available “nil rate band” (currently £325,000) subject to the availability of any exemptions and reliefs. Assets passing to spouses (or civil partners) who are also LTR will be exempt, as will certain transfers of business and agricultural assets that meet the exemption criteria, and assets passing to qualifying UK (but not US) charities.

By contrast, US estate, gift and generation-skipping taxes have much more generous exemptions, including a $15m federal exemption. This creates stark differences in exposure.

In both jurisdictions, couples with different tax profiles face particular complications. In the UK, transfers from an LTR to a non-LTR spouse (or civil partner) only benefit from a £325,000 spouse exemption (in addition to any other available exemptions or reliefs). Similarly, in the US, the unlimited marital deduction is restricted where assets pass to a non‑US spouse and testamentary planning (e.g. including a Qualifying Domestic Trust (QDOT) in the US spouse’s Will) maybe needed to defer the estate tax exposure.

Future planned inheritance tax reforms (e.g. restricting business/agricultural reliefs from April 2026 and bringing pensions into scope from April 2027) will materially affect long‑term planning for many US individuals.

How Wedlake Bell can help

We advise internationally mobile US individuals and families on the full spectrum of UK tax, estate planning, immigration and structuring issues arising before, during and after a move to the UK. Our dedicated US/UK team works closely with leading US advisers to provide coordinated, technically robust and practical solutions — whether navigating the FIG regime, reviewing US trusts and LLCs, mitigating cross‑border tax mismatches, restructuring investments, or planning for long‑term UK residence and inheritance tax exposure. We also support clients with UK wills, real estate acquisitions, business interests and family governance, ensuring their affairs are aligned on both sides of the Atlantic. Our aim is to provide clear, strategic advice that gives US clients confidence and clarity in an evolving UK tax landscape.

Wedlake Bell LLP provides English legal and UK tax advice only.

This article is for general information purposes only and does not constitute legal advice or a comprehensive statement of the law. Specific legal advice should always be sought in relation to individual circumstances.

Meet the team: